International trade in animal products and feed

- MFA Food sec MOC

- Animal feed misc

- Change in demand for animal products worldwide

- How would reduced demand for ASFs in HICs affect food security

- USDA’s Agricultural Projections to 2031

US and EU exports do not fight significantly fight food security worldwide

The USDAs 2022 Yearbook details how basically all the US' exports of beef and dairy go to upper middle and higher income countries. Some pork goes to Honduras, Dominican Republic and Colombia, totalling just under 8% of the value of pork exports. 10.8% of US poultry goes to poorer countries, including Colombia, Vietnam, Guatamala and Angola.

How necessary is trade?

- As seen above, trade trade does not alleviate the worst food security, because most trade occurs between countries that do not have extreme levels of food insecurity.

- However, food tends to trade from high yield regions to low yield regions, that global trade does redistribute food more equitably to some extent

- The healthy, sustainable EAT Lancet diet is achievable by 86 countries (containing half the worlds population), using only domestic agricultural land. This could be improved to 95% of the world population if significant yield improvements were made. This suggests that in principle we do not need much agricultural trade in order to give the world calorie and nutrition security, whilst also being sustainable.

Exports are concentrated in a few countries

Exports of livestock products are concentrated in fewer than ten countries and regions, in particular Australia and New Zealand (dairy and sheep), the EU (dairy and pork), United States of America (beef, poultry, pork and dairy products) and Brazil (beef and poultry). India is currently the country that exports the largest volumes of beef.

Many LMICs import a lot of ASFs

- 1/3 of African countries import 20% or more of their meat Latino et al., 2020

- For example, Ghana imports 90% of livestock products

- China now comprises 70% of Uruguay’s beef exports in 2020

LMICs will import far more food in the future

The FAO estimatesthat LMICs may more than double their food imports by 2050

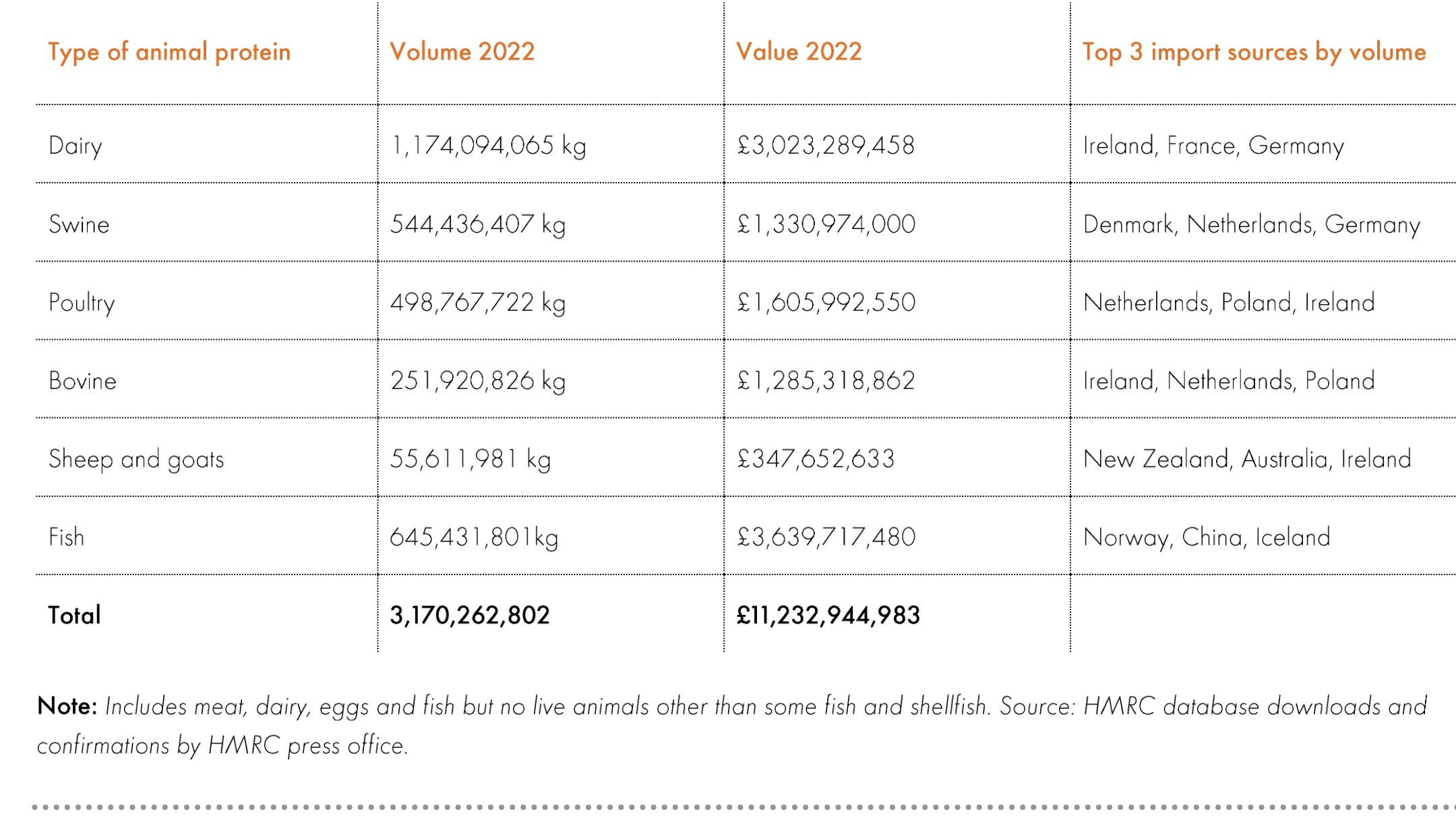

UK meat imports, 2022

Poultry trade

- poultry: India alone accounts for more than a third of the global net imports, while Indonesia and Malaysia contribute nearly 10%. (Enahoro et al., (2021))

- Exports primarily from Latin and North America

Pork trade

- China, Italy, Japan, Germany, Poland, and South Korea have been the major pork importers during the last ten years.

- Europe and North America are key exporters

- In the pork sector, according to the model projections, global exports grow by about 240% over 2010 estimates. The highest ten net exporters in 2050 account for 66% of projected 30.5 million net export quantities, with Asia as the main continental destination. the USA remains a dominant country for pork exports in 2050, contributing 32% of global quantities. Brazil (9%), Denmark, Poland and the Netherlands (~6% each), and Canada (4%) also make sizeable contributions to the global totals. China has by far the highest net import volumes (62%) of pork in 2050, driving the net import position of Asia. Other countries with reasonably high net imports are in Asia (Japan, Korea and the Philippines, ~10% of global) but also in Europe (e.g., the United Kingdom, 4%) and Africa (e.g., Nigeria, 3%). (Enahoro et al., (2021))

Beef trade

- International trade in beef is characterised mainly by net exports from the Americas, Oceania and Latin America to the rest of the world. Brazil, Argentina and Uruguay are projected to contribute 11.1 million MTs or 55% of all net beef exports. Australia is also a major net exporter at 8% of the global total in 2050, as are New Zealand and Canada (around 3% share each) (Enahoro et al., (2021))

- On a volume basis, Brazil has been the largest beef exporter in the world since 2017, followed by Australia, India, and the United States of America (USA). India’s rise in beef exports is a new phenomenon over the past decade, fuelled by rising developing country demand.

- beef will continue to be the most traded meat in the next decade (with less than 20 percent of total production currently exported). (FAO, 2016)

- Our world in data show that in the last few decades, beef consumption per capita has remained stagnant or declined for most countries.

Meat is a small part of agricultural trade but is growing

According to FAO data, around 14% of livestock production is internationally traded. Meat only makes up a small proportion of global agricultural exports, fluctuating between 5.6% and 7.5% for the last 20 years. Nonetheless it has been increasing: Between 1990 and 2018, the volume of meat exports increased by more than threefold (327%). This apparently discrepancy can be explained by the fact that non-meat food exports have grown at a similar rate.

Changing trade in South Asia

Enahoro et al., (2019) finds that South Asias demand for livestock feed will be expected to triple from 55M metric tons to 171M. Currently the region overall is not a significant importer/exporter of beef and poultry and a mild importer of dairy. By 2050 South Asia will shift to being an exporter of dairy, some 27M tons, but that this could double with targeted investments in improving dairy yields. by 2005 South Asia is also expected to become a small importer of poultry, whereas trade balance of beef is not projected to change. It should be noted that much of this change will be driven by India who dominates the South Asia region

Changing trade in SS Africa

On the other hand, Sub Saharan Africa's (SSA) demand for livestock feed is expected to double from 74M metric tons to 167M, but this could be 30-40% higher based on investments in livestock yields (presumably the spread of industrial animal farms). In terms of trade balance of animal products, SSA is similar to South Asia, being a mild importer of dairy and having a neutral balance for poultry and beef across the region (of course there could be large differences at the country level). However SSA is projected to greatly increase dairy imports by 2050 from 5.5M to 22 metric tons of dairy imported. Further, SSA is expected to need require small imports of beef and poultry to meet shortfalls in 2050 demand. Enahoro et al., (2019)

Future trade in LMICs

Overall the the results suggested that despite both South Asia and Sub Saharan Africa greatly increasing their demand for animal products, they can meet their demand through in-country production, or by trade amongst neighbouring countries within their region. This suggests that if HICs seek to export more animal products to these regions they will have to compete in the market with each country's domestic animal agricultural industries. Interestingly, dairy imports increases in SSA are projected to be around the same as export increases, suggesting that the regions could balance each other's trade, meaning there may be no change in demand for dairy from HICs.

Global trade in poultry is projected to become even more consolidated to a few countries on the export side, while imports will be more dispersed globally. In many importing countries, however, the projected changes from 2010 to 2050 are quite substantial, with potential for major disruptions to local production and/or systems supporting poultry production and consumption. (Enahoro et al., (2021))

Effect on food prices

Zhang et al., (2022) modelled what would happen to domestic and import food prices in several developing countries by 2030 undergoing rapid urbanisation and diet change (Bangladesh, China, India, and Myanmar) assuming that the rest of the world's diets change minimally. They project that Chinese domestic dairy prices could as much as double while import prices remain stable. Prices of domestically produced meat rise modestly, whilst imports again remain price-stable. This suggests that by 2030 China could be looking to import a large % of it's dairy demand and much more meat. Indian domestic meat and dairy prices will remain competitive with imports, however India will still need import more to meet rising demand.

The USDA (2021) forecasts between 2020 and 2030 almost no increase in meat consumption, However corn for animal feed is expected to grow 19%, soybeans 13%. Exports of beef pork and poultry is expected to increase by 12% but I don't know where it's being sent.

From Bryant Africa report

The majority of the African meat supply is currently made up of imports, largely from developed countries. Perversely, this imported meat is generally cheaper than meat from pastorally reared African animals, because not only is it factory farmed, it also benefits from liberal agricultural subsidies in the country of production. There are some ongoing restrictions on meat imports in our countries of interest, but most Sub-saharan countries are increasingly reliant on meat and animal products from overseas, especially as market pressures intensify. West Africa, namely Ghana, relies on nearly 90% imports.

ASF consumption in Africa in 2050

This review finds that total demand for LDF in Africa is projected to increase fourfold for meat and two to threefold for milk between 2010 and 2050, with much of this increase accounted for by population growth. Poultry meat

production, which is projected to grow the fastest of all meat types, will expand by the most in West Africa, while East Africa, the largest consumer of milk traditionally, is projected to dominate the growth of milk demand to 2050. Similarly, total demand for fish and aquatic foods is projected to grow at 30% from 2020-2050, although its consumption will fall on a per capita basis, as production in most countries will fail to keep pace with demand.

Under business-as-usual projections, imports of milk and poultry more than double by 2050, compared to 2010 levels

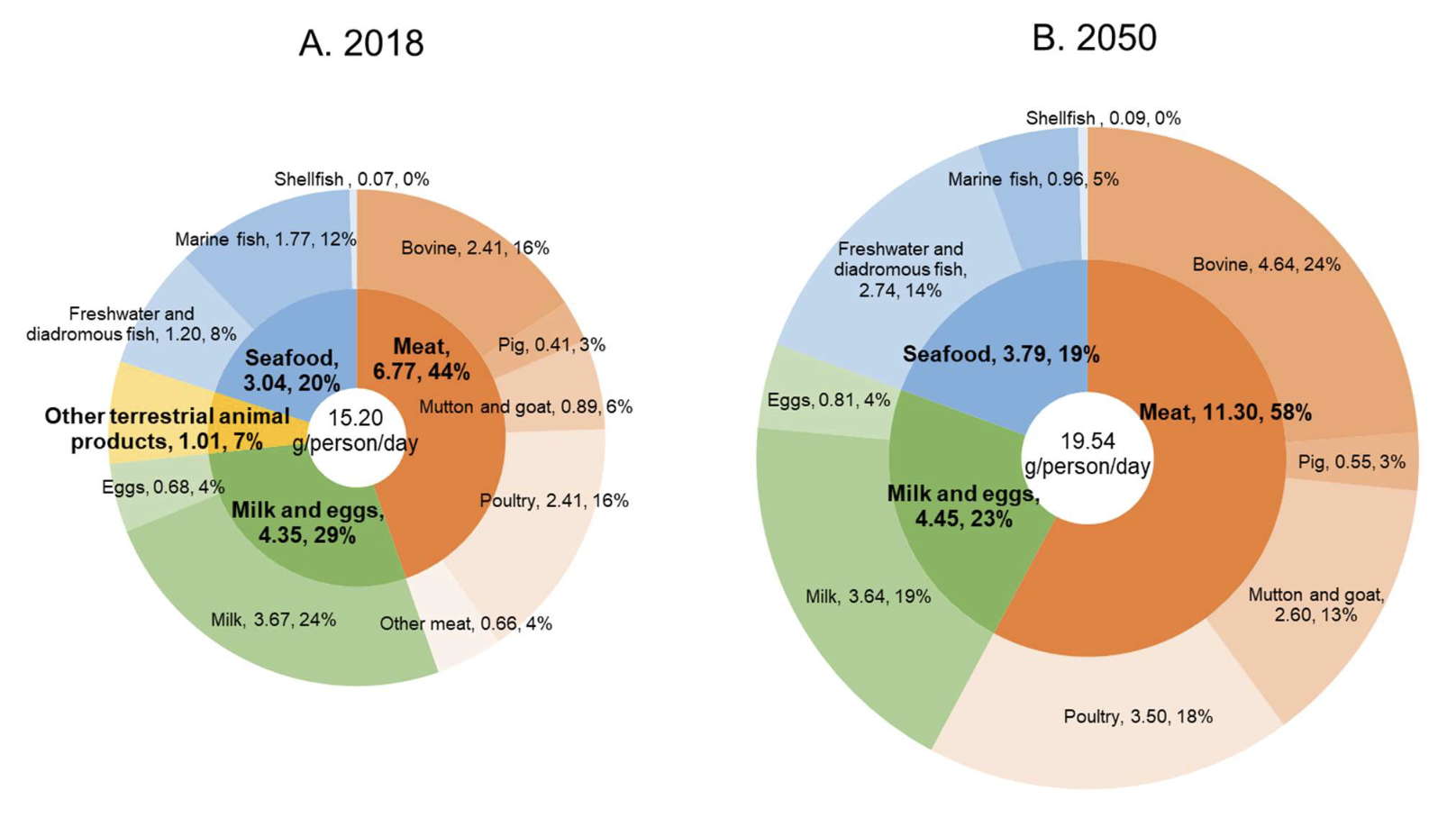

Where Africa will get its protein in 2050 compared to 2018, taken from here

According to projections from IMPACT, a widely used model of global agricultural and food systems, by 2050 the demand for meat (beef, sheep, goat, poultry, and pork combined) could reach around 221 million tonnes (MTs) in Asia and 58 million MTs in Africa. Compared to 2010, these projections represent a 77% growth in Asia and a 280% growth in Africa (Baltenweck, 2020)

Dairy

The EU is the largest producer of cow's milk in the world at 145 million tons in 2018, followed by the United States, which made 99 million tons and India, which produced 76 million tons in the same year.

However India and Pakistan, which will jointly account for over 30% of world production in 2031.

Feed trade

In 2018 57% of the UK's soy bean imports came from Argentina (who produce 11% Ritchie, 2021), next highest was Netherlands at 15% (and half of that was grown in Lat Am). including Paraguay and Brazil we get 71% of soy imports from Lat Am.

The world’s top users of cereals for feed are the USA and China, which together are responsible for 38% of the global cereal use for feed.

Japan, Spain and Mexico are the largest cereal importers for feed

Ritchie, 2021 for soy productions figures

Other

Chung and Liu (2022) find that international food trade (not just ASFs) can benefit biodiversity, because low income biodiversity hotspots are increasingly importing food from higher income countries and lower biodiversity, low income countries.

Golub et al., 2012 argue that there is a risk that taxing carbon in rich countries will just mean that livestock gets outsourced to developing countries, except if we also invest in forest credits for developing countries